Why Most People Accidentally Owe Taxes on a Rollover

401k rollovers have gotten complicated with all the bad advice flying around. Probably should have opened with this section, honestly — most rollover articles skip straight past the part that actually costs people money.

Here’s the scenario that keeps me up at night: You leave your job, get a check for $50,000, plan to drop it into an IRA within a few weeks. Straightforward, right? Then the tax bill shows up.

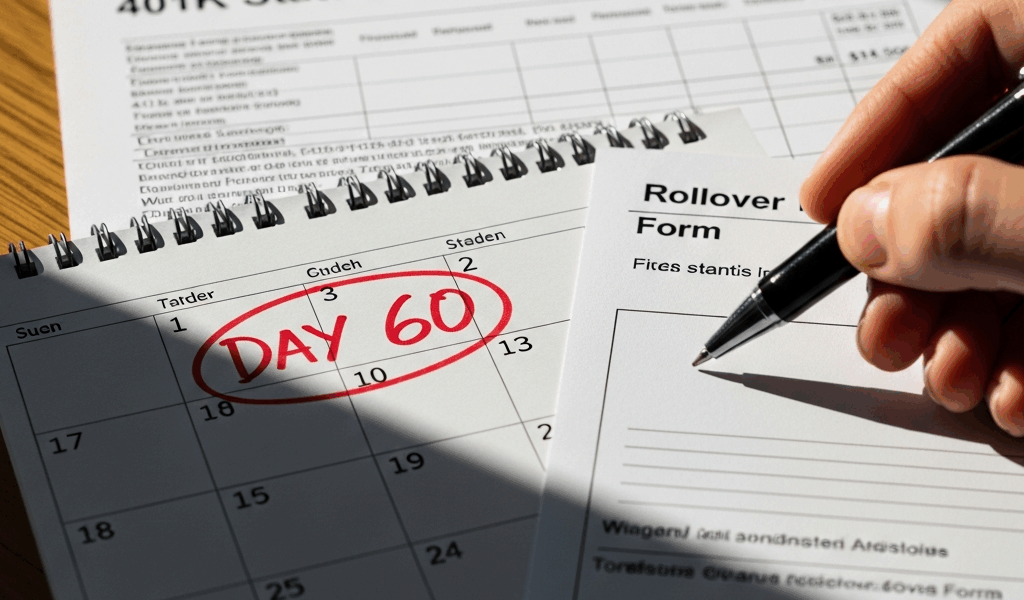

What went wrong? You triggered something called an indirect rollover. The IRS automatically withheld 20 percent federal tax the moment that check was cut. That’s $10,000 gone before you touched it. But here’s the trap — the IRS still expects you to deposit the full $50,000 into your new account within 60 days. Not $40,000. The whole fifty.

So now you’re scrambling to find $10,000 out of pocket just to avoid a tax hit. Miss that deadline or come up short, and the IRS treats the difference as a taxable distribution. Under 59.5? Add a 10 percent early withdrawal penalty on top. On a $50,000 rollover, that’s $5,000 in penalties alone — before ordinary income tax enters the picture.

Don’t make my mistake. I mailed a rollover check on day 58 of my window. It cleared on day 63. The IRS counted me as late. That’s the kind of thing nobody warns you about until after it happens.

Direct vs Indirect Rollover — Pick the Right One

Two paths exist. Only one keeps your money intact.

Direct rollover: Your old plan administrator sends the check straight to your new custodian. Never touches your hands. Zero withholding. Zero tax event. This is what you want — full stop.

Indirect rollover: The check comes to you personally. The plan is legally required to withhold 20 percent for federal taxes right away. You then have 60 days to deposit 100 percent of the original balance into a new account. The withheld amount eventually comes back to you — credited against your tax bill — but only if you complete the rollover correctly. That’s a lot of “ifs.”

That’s what makes the direct rollover so appealing to those of us who’ve been burned before. So, without further ado, here’s exactly what to say when you call your old plan administrator: “I’m requesting a direct trustee-to-trustee rollover to [new custodian name]. Please make the check payable to [new custodian name] FBO [your name], not to me personally.”

FBO means “for the benefit of.” That phrase signals to the plan that you understand the distinction — and it’s the single line item that prevents the IRS from treating the funds as a distribution to you.

The 60-Day Rule and What Happens If You Miss It

If you do take an indirect rollover — or if you’ve inherited an IRA that needs to roll over — the clock starts the moment that check is issued. Not received. Not deposited. Issued. Sixty days from that date to get the full original balance into a qualified account.

And the deposit date? That’s when funds actually clear into the new account. Not when you mail the check. Not when you submit the transfer request online. I’m apparently someone who learned this distinction the expensive way, and mailing a check two days early was absolutely not enough buffer.

Miss the deadline and the entire distribution becomes taxable income for that year. If you’re younger than 59.5, the 10 percent early withdrawal penalty applies to the whole amount. On a $50,000 rollover, that’s $5,000 in penalties plus ordinary income tax on $50,000. A $10,000 withholding mistake quietly becomes a $20,000+ tax bill.

The IRS does grant waivers — hospitalization, natural disaster, custodial delays genuinely beyond your control. But what is a hardship waiver, really? In essence, it’s a last resort. But it’s much more than that — it’s an uphill burden-of-proof situation with no guaranteed outcome. Don’t build it into your plan.

Step-by-Step — How to Complete a Tax-Free Rollover

- Contact your old plan and request a direct rollover. Call the plan administrator or log into the online portal. Ask explicitly for a direct trustee-to-trustee rollover. Request the check be made payable to the new custodian FBO your name. Write down the confirmation number — you’ll want it later.

- Choose your receiving account type. Traditional 401k balances roll into traditional IRAs. Roth 401k balances roll into Roth IRAs. Do not mix account types unless you intend to pay income tax on the conversion and actually understand why you’re doing it. Mismatched rollovers trigger immediate tax liability — no grace period, no warnings.

- Get the new custodian’s exact account details. Call your new IRA provider or brokerage. Ask for wire instructions or the mailing address for the direct rollover check. Confirm the account number and verify it’s a rollover account, not a regular IRA. These are different things and the distinction matters.

- Confirm the check payee line before it’s issued. Call your old plan back. Verify the payee reads “[New Custodian Name] FBO [Your Name]” — not your personal name. First, you should do this even if you already asked once — at least if you want to avoid a distribution event showing up on your 1099-R.

- Follow up after 10 business days. Contact your new custodian and confirm funds arrived and posted. Keep the confirmation email. That’s your proof the rollover completed within the window, in case questions come up at tax time.

One thing worth flagging: rolling a traditional 401k into a Roth IRA means you will owe income tax on the converted amount. That’s intentional — you’re paying now for tax-free growth later. But calculate that bill before committing. It’s due by April 15 of the following year, and it can be substantial depending on your bracket.

Common Rollover Mistakes That Trigger a Tax Bill

- Depositing into the wrong account type: A traditional 401k balance landing in a Roth IRA without acknowledging the tax consequence means an unexpected income tax bill — sometimes a large one. Verify the account type before the check is ever issued.

- Missing the one-rollover-per-year rule: You’re allowed one IRA-to-IRA rollover per 12-month period. The IRS counts by rolling 12 months, not calendar year. Exceed this limit and the second rollover becomes a taxable distribution, full stop. Direct rollovers don’t count against this limit — another reason to use them whenever possible.

- Rolling over company stock without thinking about net unrealized appreciation: If your 401k holds employer stock with significant embedded gains, rolling it over might cost you more than you expect. Under NUA rules, you can withdraw those shares in kind, pay ordinary income tax only on the original cost basis, and have any gains taxed at lower capital gains rates when you eventually sell. Skip this and the tax advantage disappears entirely.

- Forgetting to roll over the full balance: Some plans will let you leave small amounts behind — a few hundred dollars, sometimes more. Anything left behind is treated as a distribution. Subject to withholding, subject to penalty if you’re under 59.5. Confirm with your old plan that the entire balance is moving over, not just most of it.

Stay in the loop

Get the latest wealth rollover updates delivered to your inbox.